Why asset protection matters: safeguard your wealth in 2026

Most homeowners and small business owners believe their insurance and basic security measures fully protect their assets, but sublimits on valuables can slash theft payouts by 80% or more. Without proper documentation, legal structures, and proactive planning, you risk losing substantial wealth to creditors, lawsuits, or even minor tax debts. This guide reveals the hidden gaps in typical protection strategies and shows you practical steps to secure your home equity, business assets, and valuables against theft, liability claims, and financial risks in 2026.

Table of Contents

- Understanding The Risks To Your Assets

- How Insurance Coverage Influences Asset Protection

- Protecting Business Assets: Legal Structures And Proactive Planning

- Practical Steps To Safeguard Your Assets In 2026

- Find Reliable Asset Protection Solutions Today

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Insurance sublimits reduce coverage | Many policies cap payouts for jewelry, art, and collectibles far below actual value. |

| Documentation proves ownership | Photos and receipts are essential to support theft claims and avoid denials. |

| Legal structures shield personal wealth | LLCs and corporations separate business liabilities from your personal assets. |

| Proactive planning prevents challenges | Implementing protection before legal issues arise ensures strategies remain valid. |

| Tax foreclosure threatens home equity | Understanding exemption requirements prevents loss of substantial equity over small debts. |

Understanding the risks to your assets

Your assets face more threats than you might realize. Homeowners policies provide coverage for theft, but sublimits on certain belongings can substantially reduce coverage, leaving you with a fraction of what your valuables are actually worth. A $5,000 jewelry sublimit means even if thieves steal $30,000 in pieces, you’ll only recover that capped amount. Without proper documentation like photos and receipts, insurers can deny or severely underpay your claim, arguing you never owned the items or overstated their value.

Property owners also face legal and tax risks that can wipe out wealth overnight. Home equity theft via tax foreclosure can cause homeowners to lose substantial equity over small debts, with governments seizing entire properties worth hundreds of thousands for unpaid bills of just a few thousand dollars. Business owners encounter liability exposures from accidents on their property or lawsuits related to operations. If you operate without proper legal separation, creditors can pursue your home, savings, and personal belongings to satisfy business debts.

Recognizing these vulnerabilities is your first defense. Common risks include:

- Theft claims denied due to lack of proof of ownership or value

- Liability lawsuits from slip-and-fall accidents or professional errors

- Business creditors seizing personal assets when no legal structure exists

- Government foreclosures over unpaid property taxes or liens

Understanding these risks is the first step toward effective protection. Once you know where you’re vulnerable, you can build home valuables protection strategies that address each threat systematically.

The gap between perceived and actual protection is where most people lose money. You might assume your standard homeowners policy covers everything, but reading the fine print reveals dozens of exclusions and caps. Similarly, running a business as a sole proprietor feels simple until a lawsuit threatens your family home. Closing these gaps requires intentional planning, proper insurance structure, and legal protections that separate your personal wealth from business risks.

How insurance coverage influences asset protection

Insurance forms the foundation of asset protection, but only when structured correctly. Photographic documentation and purchase receipts help prove ownership and support theft claims, giving insurers the evidence they need to process payouts quickly. Create a digital inventory with photos of every valuable item, including serial numbers, appraisals, and original purchase documents. Store this documentation in cloud storage or a safe deposit box so it survives the same disaster that might damage your property.

Review your policy declarations page carefully to identify sublimits that cap coverage for specific categories. Standard policies often limit jewelry to $1,500, silverware to $2,500, and collectibles to similar low amounts. You can purchase riders or floaters that extend coverage to full replacement value for these items, typically for a small additional premium. The cost of a rider is minimal compared to the financial loss you’d face trying to replace valuable items out of pocket after a theft.

Insurance must reflect correct ownership titling, such as naming a trust as additional insured, ensuring coverage remains valid even when assets are held in legal structures designed for estate planning or liability protection. If you transfer your home to a trust but fail to update the insurance policy, a claim could be denied because the named insured no longer matches the property owner. This administrative detail can cost you everything in a total loss scenario.

Your insurance strategy should also address liability and disaster risks specific to your location. Coverage should include liability protection and region-specific natural disasters, such as flood insurance in coastal areas or earthquake coverage in seismic zones. Liability limits of $300,000 might seem adequate, but a serious accident can generate medical bills and legal judgments far exceeding that amount. Consider umbrella policies that extend liability coverage to $1 million or more for relatively low premiums.

Pro Tip: Schedule an annual insurance review every January to update coverage as you acquire new valuables, adjust for inflation, and ensure all ownership entities are correctly listed on policies.

Key insurance actions to protect assets:

- Photograph all valuables with serial numbers visible and store documentation securely

- Add scheduled riders for items exceeding sublimits in your standard policy

- Update policies to reflect trusts, LLCs, or other ownership structures

- Purchase umbrella liability coverage to extend protection beyond base limits

- Verify disaster coverage matches your geographic risks

| Coverage Type | Standard Limit | Recommended Action |

|---|---|---|

| Jewelry | $1,500 | Add rider for full appraised value |

| Fine Art | $2,500 | Schedule individual pieces over $1,000 |

| Electronics | $5,000 | Document serial numbers and receipts |

| Liability | $300,000 | Purchase $1M+ umbrella policy |

Understanding how security standards in asset protection work alongside insurance helps you build layered defenses. Physical security reduces the likelihood of theft, while proper insurance ensures financial recovery if prevention fails. Both elements must work together for comprehensive protection.

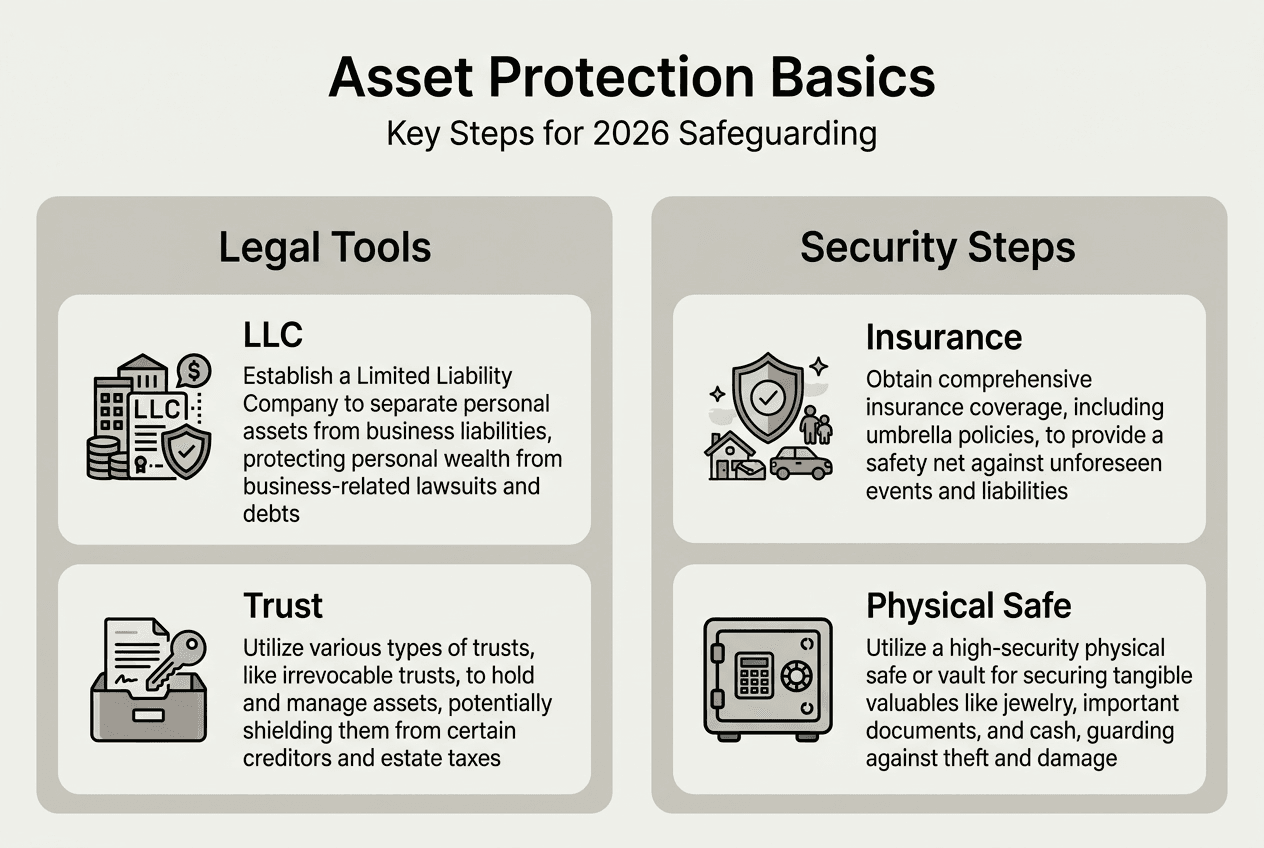

Protecting business assets: legal structures and proactive planning

Asset protection is crucial for business owners to shield wealth from lawsuits and creditors, creating legal barriers that prevent personal assets from being seized to satisfy business obligations. Operating as a sole proprietor or general partnership offers no separation between business and personal liability. If someone sues your business or a vendor seeks payment, they can pursue your home, car, and savings accounts directly.

LLCs are a widely used structure to separate personal assets from business liabilities, creating a legal entity that owns business assets and assumes business debts. When properly maintained, creditors can only pursue assets owned by the LLC itself, not your personal wealth. This protection is called the “corporate veil,” and it remains intact as long as you follow formalities like keeping separate bank accounts, maintaining corporate records, and avoiding commingling personal and business funds.

Corporations offer similar protections with different tax treatments and governance structures. S corporations and C corporations both shield personal assets from business liabilities, but they require more administrative overhead than LLCs. The choice depends on your business size, growth plans, and tax situation. Many small business owners find LLCs provide adequate protection with simpler compliance requirements.

Pro Tip: Form your LLC or corporation before you need it. Asset protection is most effective when implemented proactively before legal or financial issues arise, because transfers made after a lawsuit is filed or debt becomes due can be reversed as fraudulent conveyances.

Timing matters enormously in asset protection. Courts scrutinize transfers made when legal threats are imminent, often unwinding them and exposing assets you tried to protect. Establishing structures years before problems arise demonstrates legitimate business and estate planning purposes rather than attempts to defraud creditors. This proactive approach ensures your protections withstand legal challenges.

Consider how different structures compare for asset protection:

| Business Structure | Personal Liability Protection | Setup Complexity | Annual Maintenance |

|---|---|---|---|

| Sole Proprietorship | None | Minimal | Low |

| General Partnership | None | Low | Low |

| LLC | Strong | Moderate | Moderate |

| S Corporation | Strong | High | High |

| C Corporation | Strong | High | High |

Integrating asset protection with estate and financial planning creates comprehensive security. Your LLC might own business assets, while a trust holds your home and investment accounts, and insurance covers liability risks. Each layer addresses different threats, and together they form a robust defense against creditors, lawsuits, and financial disasters. Working with legal and financial professionals helps you design structures appropriate for your specific situation and risk profile.

Exploring business asset protection strategies reveals how physical security measures complement legal protections, creating multiple barriers against loss. Understanding the importance of asset protection investment helps you prioritize spending on structures and systems that deliver measurable risk reduction.

Practical steps to safeguard your assets in 2026

Taking action now protects your wealth before problems arise. Policyholders should review their insurance policy declarations page to understand coverage limits and sublimits, identifying gaps that leave valuables underinsured. Pull out your policy documents and create a spreadsheet listing each coverage category, its limit, and the actual value of items in that category. Where gaps exist, contact your insurance agent to add riders or increase limits.

Follow these steps to implement effective asset protection:

- Document everything you own with photos, receipts, and appraisals stored in multiple secure locations including cloud backup.

- Review insurance policies annually to adjust coverage for new purchases, inflation, and changes in ownership structure.

- Establish an LLC or corporation for your business operations before legal or financial problems emerge.

- Separate personal and business finances completely with dedicated bank accounts and credit cards.

- Verify property tax exemptions are properly filed to avoid foreclosure over administrative errors.

- Create an asset protection plan that integrates insurance, legal structures, physical security, and estate planning.

- Update your plan whenever you acquire significant assets, start new business ventures, or face increased liability risks.

Asset protection strategies should be implemented proactively and integrated with estate and financial planning, creating a comprehensive approach that addresses multiple threats simultaneously. Don’t wait until you’re facing a lawsuit or financial crisis. Protections established under duress can be challenged and unwound by courts, leaving you exposed despite your efforts.

Property tax issues deserve special attention because they can result in catastrophic losses. Understanding and meeting property tax exemption requirements can prevent unexpected foreclosures, saving homeowners from losing hundreds of thousands in equity over relatively small debts. Contact your county assessor’s office to verify all exemptions you’re entitled to are properly recorded. Set up automatic reminders for tax payment deadlines, and if you face financial hardship, explore payment plans before falling into default.

Pro Tip: Create a master asset protection checklist that you review quarterly, covering insurance adequacy, legal structure compliance, documentation updates, and tax obligation status. This systematic approach catches problems before they become crises.

Physical security measures complement legal and financial protections. High-quality safes protect valuables from theft and fire, surveillance systems deter criminals and provide evidence for claims, and access controls limit who can reach your most valuable assets. Following an asset protection workflow guide helps you implement security systematically rather than reacting to individual threats as they emerge.

Your protection strategy should evolve as your wealth grows and risks change. Review and update your approach annually or whenever major life events occur like starting a business, purchasing property, or receiving an inheritance. Laws governing asset protection vary by state and change over time, so staying informed ensures your strategies remain effective and compliant. Understanding your business security needs helps you allocate resources to the most critical vulnerabilities first.

Find reliable asset protection solutions today

Protecting your assets requires more than insurance and legal structures. Physical security creates an essential layer of defense that prevents losses before they occur. Quality safes protect your most valuable possessions from theft and fire, giving you peace of mind that important documents, jewelry, and collectibles remain secure even during disasters. Surveillance systems and access controls add additional barriers that deter criminals and limit exposure.

Safes and Security Direct offers professional-grade security solutions designed specifically for homeowners and small business owners who take asset protection seriously. Explore fire-resistant safes that preserve irreplaceable documents and valuables, burglary-resistant models that withstand determined attacks, and commercial-grade systems that secure business assets around the clock. Every product is engineered to meet rigorous security standards, ensuring reliable protection when you need it most.

Start building comprehensive protection today by reviewing asset protection solutions that complement your insurance and legal strategies. Discover business asset protection strategies that secure commercial assets and explore home valuables protection strategies tailored for residential security needs. Your wealth deserves protection that works.

Frequently asked questions

Why is asset protection important for homeowners?

Asset protection prevents the loss of home equity and personal wealth to creditors, lawsuits, and government seizures. Without proper planning, a single liability claim or tax foreclosure can wipe out years of savings and force you to liquidate your most valuable possessions. Proactive measures like adequate insurance, proper documentation, and physical security create barriers that preserve your wealth through unexpected challenges.

How can I prevent losses from sublimits in home insurance?

Review your policy declarations page to identify categories with sublimits, then purchase scheduled riders that extend coverage to full replacement value for specific high-value items. Document each valuable with photos, appraisals, and receipts to support claims. This small additional premium investment prevents devastating financial losses when theft or disaster strikes.

What documentation is best for proving ownership of valuables?

Photographs showing items with visible serial numbers, original purchase receipts, professional appraisals, and certificates of authenticity provide the strongest proof of ownership and value. Store digital copies in cloud services and physical copies in a safe deposit box or fireproof safe. Update your inventory annually as you acquire new valuables or dispose of old ones.

How does forming an LLC protect my personal assets?

An LLC creates a separate legal entity that owns business assets and assumes business liabilities, preventing creditors from pursuing your home, savings, and personal property to satisfy business debts. This protection remains valid as long as you maintain corporate formalities like separate bank accounts, proper record keeping, and avoiding commingling of personal and business funds.

What are the risks of tax foreclosure and how can I avoid them?

Governments can seize your entire property over unpaid tax bills worth a fraction of your home’s value, causing you to lose substantial equity. Verify all property tax exemptions are properly filed with your county assessor, set automatic payment reminders, and explore payment plans immediately if you face financial hardship. These simple steps prevent catastrophic losses over administrative errors or temporary cash flow problems.

When should I start implementing asset protection strategies?

Begin asset protection planning immediately, before legal threats or financial problems emerge. Courts scrutinize transfers made after lawsuits are filed or debts become due, often unwinding them as fraudulent conveyances. Establishing protections years in advance demonstrates legitimate planning purposes and ensures your strategies withstand legal challenges when you need them most.

Recommended

- Why invest in asset protection: cut risks by 40% in 2026 – Safes and Security Direct

- Asset Protection Strategies 2026: Safeguard Your Business Assets – Safes and Security Direct

- Top Asset Protection Methods 2026 for Secure Homes – Safes and Security Direct

- How to protect valuables at home: strategies for 2026 – Safes and Security Direct